This paper provides a novel dataset of time-varying measures on the degree of countercyclicality of fiscal policies for advanced and developing economies between 1980 and 2021. The use of time-varying measures of fiscal stabilization, with special attention to potential endogeneity issues, overcomes the major limitation of previous studies and allows the analysis to account for both country-specific as well as global factors. The paper also examines the key determinants of countercyclicality of fiscal policy with a focus on factors as severe crises, informality, financial development and governance. Empirical results show that (i) fiscal policy tends to be more countercyclical during severe crises than typical recessions, especially for advanced economies; (ii) fiscal countercyclicality has increased over time for many economies over the last two decades; (iii) discretionary and automatic countercyclicality are both strong in advanced economies but acyclical (at times procyclical) in low-income countries; (iv) fiscal countercyclicality operates primarily through the expenditure channel, particularly for social benefits; and (v) better financial development, larger government size and stronger institutional quality are associated with larger countercyclical effects of fiscal policy. Our results are robust to various specifications and endogeneity checks.

Avoid common mistakes on your manuscript.

Views on the appropriate fiscal response to adverse events have been reshaped by the experience gained during severe crises. Before the global financial crises, discretionary fiscal responses were deemed too slow or hard to unwind (Blanchard et al. 2010; Blinder 2016), and automatic stabilizers—built-in mechanism in the budget that raises spending or reduces revenue collection during adverse shocks—were considered sufficient. During the unprecedented global shock of the pandemic, political consensus made it possible to deploy even more rapid, diverse and novel measures. Fiscal interventions during the global financial crisis shored up private sector balance sheets and stimulated aggregate demand at a time when monetary policy in advanced economies was constrained. These suggest that fiscal policy can be swift and forceful during crises, pointing to a possible greater stabilization role of fiscal policy than in typical recessions.

The experience during recent severe crises have therefore led to a reassessment of fiscal responses. Policy debate has focused not only on the appropriate size and efficient stabilization mechanism, but also on how to improve the balance between discretionary versus automatic fiscal stabilizers. In the face of increasing constraints on discretionary fiscal policy (from debt sustainability problems, fiscal space limitations, financial market pressures or the presence of fiscal rules), a reassessment of the balance between discretionary and automatic fiscal stabilization comes timely.

The focus of this paper is the assessment of the degree of fiscal policy countercyclicality across time, countries and crisis episodes and the analysis of its determinants. We say that fiscal is countercyclical if the budget balance (-to-GDP ratio) increases when output growth increases and falls when output growth declines. Similarly, looking at the components of the budget balance, we say that government spending (revenue) is more countercyclical if, as a share of GDP, it increases more (less) for any given reduction in GDP growth. Fiscal countercyclicality is an interesting property to study because it is intimately linked to a broader problem, whose full exploration is, however, beyond the scope of this paper: the ability of fiscal policy to provide macroeconomic stabilization. Fiscal stabilization can work through several different channels. For example, countercyclical “automatic stabilizers” are proactive fiscal tools that automatically smooth economic activity (Baunsgaard and Symansky 2009; Jalles, 2020). Footnote 1 But even passive policies, such as keeping government expenditure fixed in absolute terms independently of the stage of the cycle, are countercyclical by our definition and can therefore have a stabilizing effect. On the other hand, discretionary fiscal measures can, in some cases, turn out to have a procyclical bias and therefore a destabilizing effect (van den Noord 2000).

Previous empirical studies recognize the difficulties in providing accurate estimates of fiscal stabilizers, but they also acknowledge the need to have at least approximations of it (Cotis et al. 1996; Auerbach and Feenberg 2000). This paper tries to answer these questions using a novel empirical strategy and estimating time-varying measures of fiscal countercyclicality for an unbalanced panel of advanced and emerging market and developing economies from 1980 to 2021. The use of time-varying measures of fiscal countercyclicality overcomes the major limitation of existing studies assessing the determinants of fiscal stabilization that rely on cross-country regressions and therefore are not able to account for country-specific as well as global factors. The key findings of the paper are as follows: (i) fiscal countercyclicality has increased over time for many economies over the last two decades, (ii) countercyclicality tends to be relatively stronger during severe downturns, especially in advanced economies, (iii) previously estimated countercyclicality coefficients are likely to be lower bounds, (iv) the discretionary and automatic components of the budget balance display countercyclical effects for advanced economies, but are not pinpointed in a statistically significant way for emerging market economies and low-income developing countries, (v) fiscal countercyclicality operates primarily though the expenditure channel, with social security benefits being the most countercyclical component, and (vi) financial development, government size and institutional quality matter, particularly for automatic stabilizers.

The remainder of the paper is organized as follows. Section II provides a relevant literature review. Section III presents a conceptual framework and an empirical strategy for estimating the static and time-varying measures of fiscal countercyclicality and analyzing their key determinants. Section IV discusses the main empirical findings and related extensions and results of the robustness checks. The last section concludes.

The two major crises of the past decade and a half have led to a reassessment on the role of fiscal policy in stabilizing output. During the COVID-19 pandemic, fiscal support was swift and impactful. Novel and diverse measures were deployed beyond the automatic stabilizers (IMF 2022, Auerbach et. al. 2022; Bouabdallah et al. 2020). Before the global financial crisis, discretionary fiscal responses were considered too slow or hard to unwind (Blanchard, Dell’Ariccia, and Mauro 2010; Blinder 2016). Automatic stabilizers are often perceived sufficient to deliver timely, targeted and temporary support and should have those fully operational. Most policies focus on strengthening automatic stabilizers to stabilize cyclical fluctuations.

The countercyclical properties of fiscal policy vary between automatic stabilizers and discretionary policies and across countries. Many studies conclude that the two components (automatic stabilizers and discretionary policy) are not mutually exclusive, although countries that have stronger automatic stabilizers are less likely to enact substantive discretionary fiscal measures during typical recessions (Dolls et al. 2012a, b). Different approaches are often used to estimate the size of automatic stabilizers. One way is to apply the overall cyclical sensitivity of the budget using reduced-form semi-elasticities for revenue and expenditure categories with respect to the output gap (e.g., Girouard and André 2005; Baunsgaard and Symansky 2009; Fedelino et al. 2009; Mohl et al. 2019; Mourre and Princen 2019). Footnote 2 Footnote 3 Some studies also use the micro-simulation approach to measure the size of automatic stabilizers of the tax and benefit system by assessing how a hypothetical income shock would affect household disposable income (after taxes and benefits) based on household-level surveys and detailed information of the tax and benefit systems (Pechman 1973, 1987; Knieser and Ziliak 2002; Auerbach 2009; Dolls et al. 2012b). Dolls et al. (2012b) find that automatic stabilizers have absorbed nearly 40 percent of a proportional income shock in the EU countries, compared to 32 percent in the USA, while the stabilizing effects appear much higher during the COVID-19 pandemic if considering the effects of job retention schemes existing in many EU countries (Lam and Solovyeva 2022) Footnote 4 An alternative approach is to calibrate a general equilibrium macro model to assess the aggregate relationship between the government budget and the output gap, which in turn, provides the basis to assess the size of the automatic stabilizers (Fedelino et al. 2005; Fatas and Mihov 2012; McKay and Reis 2016, 2019). This has an advantage to illustrate various channels how automatic stabilizers can reduce economic volatility, including (i) the disposable income channel (Brown 1955); (ii) the marginal incentives channel (Christiano 1984); (iii) the redistribution channel (Blinder 1975; Oh and Reis 2012); and (iv) the social insurance (or wealth distribution) channel (Floden 2001; Alonso-Ortiz and Rogerson 2010; Challe and Ragot 2015). Footnote 5 Automatic stabilizers are typically stronger and more effective in high-income countries and in those countries with more developed financial systems and fiscal rules (IMF 2015a, b). There is evidence of a secular decline in the role of automatic stabilizers in the USA since their historical peak in the 1970s (see Auerbach 2008). But more recent data point an increased role of automatic stabilizers during the pandemic (Bouabdallah et al. 2020).

The literature also finds the role of fiscal stabilization varies and depends on different factors. Seidman and Lewis (2002) present a new design for automatic fiscal policy and use the Fair US quarterly model to test it. They find that during severe downturns, monetary policy alone does not suffice for macroeconomic stabilization. But monetary policy combined with the proposed automatic fiscal policy substantially can reduce the severity of the recession without generating a sizeable increase in public debt. More recently, Jalles (2020) using a panel dataset found additionally that the fiscal response to demand shocks is higher than to supply shocks and that accounting for future expectations about fiscal dynamics enhances the degree of fiscal countercyclicality. Furceri and Jalles (2019) used a difference-in-difference approach to 25 industries for 18 advanced economies over the period 1985–2012 to examine the effect of fiscal countercyclicality on productive investment. Results show that fiscal countercyclicality increases research and development (R&D) expenditure and the share of information, capital and technology (ICT) capital in industries that are more financially constrained. Furceri, Choi and Jalles (2022) applied a difference-in-difference approach to an unbalanced panel of 22 manufacturing industries for 55 countries to find that the credit constraints channel identifies the best transmission mechanism through which countercyclical fiscal policy enhances growth.

This strand of the literature also assesses the determinants of fiscal stabilization using time-varying measures focusing on a subset of advanced economies (Aghion and Marinescu 2008). Several studies in the literature that have performed a similar analysis using cross-country regressions for a large set of advanced and emerging market economies. Concerning the determinants of fiscal countercyclicality, government size has typically been found to be the most important driver (Gali 1994; Debrun et al. 2008; Debrun and Kapoor 2011; Furceri 2010; Afonso and Jalles 2013). Another important determinant of fiscal countercyclicality is the degree of openness: Economies that are more open to trade tend to be more exposed to external shocks and may use more actively fiscal policies in order to provide increased stabilization (Rodrik 1998; Lane 2003). Similarly, capital account openness is found to affect fiscal stabilization as foreign capital tends to flow in (out) during expansions (recessions), therefore increasing the cost of financing countercyclical fiscal policies (Aghion and Marinescu 2008). Studies have also found higher fiscal stabilization in more developed countries, as these tend also to be characterized by better institutions (or of higher quality) and by higher levels of financial development (Talvi and Vegh 2005; Frankel et al. 2011; Acemoglu et al. 2013; and Fatas and Mihov 2013). Jalles (2018) looking at determinants of fiscal countercyclicality found that fiscal rules contribute to its reduction and that the result is especially strong for debt-based rules in advanced economies. Stronger automatic stabilizers are associated with larger government size (Gali 1994; Rodrik 1998; Fatas and Mihov 2001). For instance, Fatas and Mihov (2001) find that one percentage point increase in government size relative to GDP reduces output volatility by eight basis points. However, beyond a certain level, government size may have sizeable efficiency costs. Footnote 6

Fiscal countercyclicality and stabilization are two distinct but tightly related concepts. In fact, we can think about the degree of fiscal stabilization in terms of the product between the degree of fiscal countercyclicality and the “multiplier” effect of fiscal policy on the real economy. Then, keeping fixed the multiplier effect of fiscal policy, higher fiscal countercyclicality automatically translates into higher fiscal stabilization. This is an argument that has often been adopted in the literature (see the discussion sin Blanchard 1993; Lane 2002; Fatás and Mihov 2012).

This section lays out a simple methodological framework that provides an explicit relation between fiscal countercyclicality and fiscal stabilization and presents a precise interpretation of the empirical estimations carried out in the rest of the paper. We begin by presenting a general form for our main estimation equation,

$$where \(_\) is a fiscal variable that signal an improvement in public finances (e.g., budget balance, fiscal revenues, the negative of government expenditure) and \(_\) is a measure of economic activity. A second structural equation, the “fiscal multiplier equation,” which we do not estimate in this paper, determines the feedback loop between fiscal policy and economic activity

$$The structural shocks \(_^\) and \(_^\) are assumed to be uncorrelated with each other and have finite and strictly positive variance \(_^\) and \(_^\) , respectively. The parameter \(\beta\) in gives the degree of countercyclicality of fiscal policy, whereas \(\delta\) in is the fiscal multiplier. In this paper, we maintain the reasonable hypothesis that \(\delta\) >0. Solving the above system of two equations gives

$$We define the degree \(\Sigma\) of fiscal policy stabilization as the counterfactual standard deviation of economic activity \(_\) if \(\beta =0\) (i.e., if fiscal policy were unresponsive to economic conditions) relative to the standard deviation of \(_\) under given policy parameters \(\beta\) and \(\delta\) and obtain

$$\Sigma =1+\delta \beta$$The equation above shows that for a given positive fiscal multiplier \((\delta >0)\) , the degree of fiscal stabilization \(\Sigma\) increases with the degree \(\beta\) of countercyclicality. An OLS estimate of the main equation defining \(\beta\) (first equation above) suffers from a simultaneous equation bias from the omission of the fiscal multiplier equation. More precisely, for \(\delta >0\) the estimate \(\widehat\) is downward biased

$$\widehat=\fracConsider splitting the estimation sample into non-overlapping intervals indicated with \(T=\mathrm,\dots ,N\) and assume the volatility of structural shocks and the size of fiscal multipliers are the same across intervals, while the degree of countercyclicality \(_\) is potentially different across intervals. Then, for two distinct intervals \(T\) and \(T<\prime>\) we have \(<\widehat>_-<\widehat>_<<\prime>>=(_-_<<\prime>>)/(1+^_^/_^)\) . Therefore, under the described assumption, the change in the (biased) OLS regressors correctly captures the direction of the change of the true parameters.

We translate the main equation defining \(\beta\) in the previous section into an empirical equation by following Blanchard (1993) and using the budget balance \(B_\) (expressed in percent of GDP) in place of \(_\) , where the additional subscript \(i\) is the label that we assign to countries in our panel estimation framework. We also use two alternative measures of economic activity \(_\) and \(_\)

$$where \(_\) is the real GDP growth rate (so \(_\) is the log of real GDP). Equation (7) assumes that fiscal policy reacts to any type of economic disturbance that affects the growth rate of the economy.

When evaluating the reaction of fiscal policy, we can distinguish between discretionary and the automatic components of the fiscal response. This distinction requires decomposing the budget balance into a cyclically adjusted ( \(CAB)\) and an automatic part. Footnote 7 We then estimate the following

$$where \(^\) and \(^\) capture the degree of the countercyclicality attributable to “discretionary” fiscal response and that attributable to automatic stabilizers, respectively. Equations 7 and 8a/8b can also accommodate a time-varying set of regression coefficients:

$$Measures of the CAB (and thus of potential output gap) are available in IMF World Economic Outlook database, but mostly for advanced economies and a few emerging markets and low-income countries. Therefore, when we estimate (8) using WEO output gaps, the sample of emerging markets and low-income countries will be somewhat limited. The relative paucity of output gap observations is, however, a problem for the next section, where we look at a relatively large number of determinants of fiscal countercyclicality. In that case, we resort to the Hamilton filtering method to obtain output gaps consistently across a wide set of countries (Borio et al. 2013, 2014). Footnote 8 More precisely, the CAB is calculated with a general application of a unity elasticity of government revenues (REV) to the output gap and inelastic expenditure (EXP) to the output gap (Girouard and André 2005). That is, CAB = REV·[1/(1 + OG/100)]—EXP.

This section describes the empirical approach to assess the determinants of the coefficients \(\) of countercyclicality obtained in Section III.A. The size of fiscal countercyclicality coefficients is related to various macroeconomic, structural, institutional and political factors. For this purpose, the following regression is estimated based on an unbalanced sample of all countries that have estimates of countercyclicality coefficients for at least 20 years (that is, at least since 2002 onwards for 20 continuous observations of \(\) coefficients, calculated with Hamilton filtered output gaps):

$$>_=_+<\gamma >_+>\boldsymbol<^<\prime>>>>_<<\varvec><\varvec>>+_^$$where \(_\) are country fixed effects to capture unobserved heterogeneity across countries and time-unvarying factors such as geography which may affect the degree of fiscal countercyclicality; \(<\gamma >_\) are time fixed effects to control for global shocks; and \(>>_<<\varvec><\varvec>>\) is a vector of time-varying macroeconomic and political variables described below (Furceri and Jalles 2018; Jalles 2020).Since the dependent variables in Eq. (10) are based on estimates, the regression residuals consist of two components: (i) sampling error (the difference between the true value of the dependent variable and its estimated value) and (ii) the random shock that would have been obtained even if the dependent variable had been observed directly. Correcting for (i) would help us reduce the overall noise and thus increase the statistical significance of our estimates. To this end, we employ a weighted least-squares (WLS) approach. Specifically, the WLS estimator assumes that the errors \(_\) in Eq. (10) are distributed as \(_\sim N(0,\frac^>_>)\) , where \(_\) are the estimated standard deviations of the fiscal countercyclicality coefficient for each country i and \(^\) is an unknown parameter. To reduce the potential bias from the reverse causality, all the explanatory variables in the regression enter the specification with one lag.

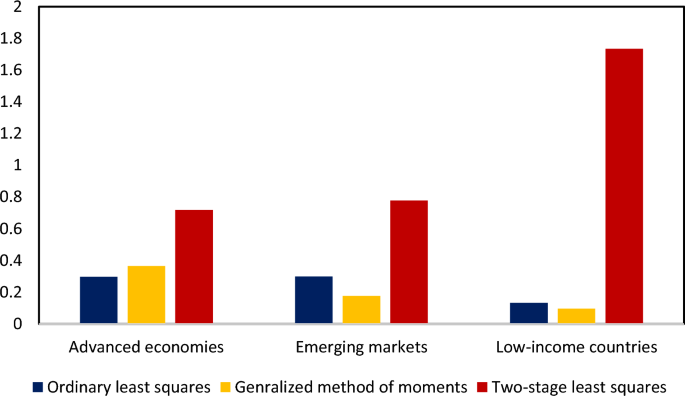

We first present our empirical results of Eq. (9) for three income groups: advanced economies (AEs), emerging market economies (EMs) and low-income countries (LICs). Footnote 25 Our sample covers about 190 countries during the period of 1980–2021 on an annual basis. Table 1 shows that, on average across countries, fiscal policy has behaved countercyclically in all income groups during the period considered. The degree of countercyclicality is increasing with the level of economic development, with advanced economies and emerging markets economies having higher estimated coefficients, compared to low-income countries. Non-commodity exporting EMs behave very similarly to non-commodity exporting LICs. In fact, excluding commodity exporters (specification 7, Table 1) suggests that fiscal countercyclicality coefficients are the highest among AEs at 0.3, while the magnitudes are only about half at 0.14 and 0.17 for EMs and LICs, respectively.

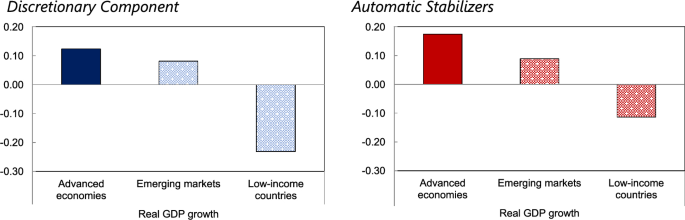

Next, we present our estimation results for Eqs. 8a and 8b. Figure 2 shows that a one percentage point growth rate change in AEs generates an increase in the automatic part of the budged balance equal to 0.17 percentage point of GDP, compared to an increase of 0.12 points for the discretionary part. The coefficients for two components, albeit not statistically significant individually, are similar in the case of EMs, while the point to a procyclical behavior for LICs. Footnote 27

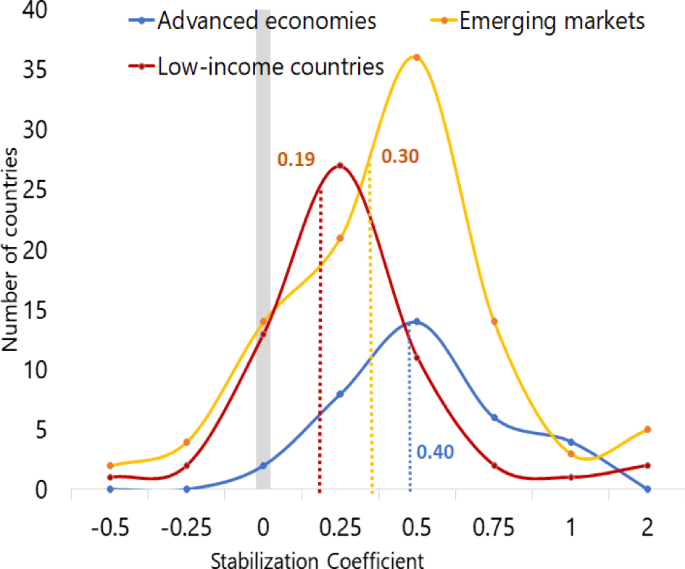

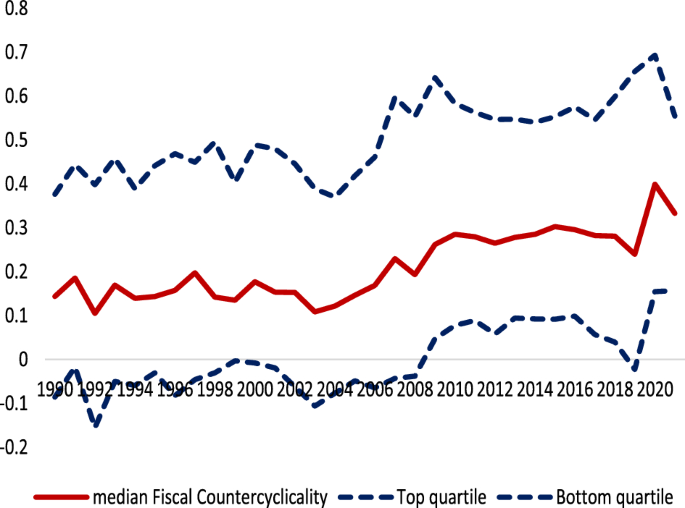

To provide a more refined picture than Table 1 on how the degree of the countercyclicality varies across countries, in Fig. 3 we estimate (1) for each country individually (only countries with at least 20 continuous observations enter the regression). The results confirm that the average degree of fiscal countercyclicality in AEs (at 0.4) is greater than that of EMEs and LICs (0.3 and 0.19, respectively). In addition, the dispersion across countries tends to be larger in EMs, with a greater density toward the lower half of the distribution, while the distribution is tilted to the higher end for advanced economies. In addition, to explore the countercyclicality over time, we estimate the panel (1) over 10-year rolling windows (Fig. 4). Footnote 28 Our estimation results also point to a slow upward trend of the countercyclicality of fiscal policy since 1990, with a more notable upward movement during 2000–10 (confirming Furceri and Jalles (2018) that used data ending in 2014). The median countercyclicality of fiscal policy rose from 0.15 in 1990 to 0.25 in 2019, before jumping to around 0.3 in 2020 at the peak of the pandemic.

In the final part of this section, we concentrate on the potential asymmetry of the degree of countercyclicality during recessions compared to the overall average sample. To this end, we group recessions into three categories: (i) typical recessions, which refer to periods when an individual country’s growth is below the country’s own average of the previous three years; (ii) global financial crisis (2008–10); and (iii) the COVID-19 pandemic (2020–21). The first panel of Fig. 5 shows that fiscal policy tends to be more countercyclical during severe crises than in normal recessions. This was particularly the case during the GFC and the COVID-19 pandemic. The second panel of Fig. 5 provides another way to look at this conclusion by calculating the share of countries in each income group that have displayed a larger countercyclical coefficient during each specific episode relative to their own average coefficient over the entire time span. More than 70 percent of AEs conducted a more aggressive countercyclical fiscal policy during the GFC and COVID-19 pandemic than in a typical recession. The majority of countries in EMs and LICs also put out stronger countercyclical responses during those crises than in a typical.

In this section, we re-estimate Eq. (7) separately for the revenue and expenditure components of the budget balance (expressed in percent of GDP). The specification is similar to Darby and Melitz (2008) that examines how the government budget and its composition respond to the output gap for 21 OECD countries during 1982–2003. The specification includes revenue components excluding grants, such as total revenue, income taxes, individual income taxes, corporate income taxes, taxes on goods and services, and taxes on international trade. On the expenditure side, the components in the specification include total primary expenditure, public investment, compensation of employees, public spending on goods and services, and social security benefits.

Empirical results show that both government revenues and expenditures as a share of GDP act countercyclically (Column 1 of Tables 2 and 3). Footnote 29 For example, a one percentage point increase in real GDP growth is estimated to increase the revenue ratio by 0.034 percentage points and decrease the expenditure ratio by 0.2 percentage point of GDP. This is entirely driven by the strong response of taxes on goods and services to changes in GDP. Also, discretionary tax policy is typically procyclical, as estimates of \(^\) are negative and statistically significant for all tax items. The countercyclicality of fiscal policy therefore operates primarily through the expenditure side, even though the sub-component of investment spending is slightly procyclical. As expected, spending components that have built-in automatic stabilizers, such as social security benefits, operate more countercyclically.

Table 2 Countercyclical properties of government revenues Table 3 Countercyclical properties of government expendituresTo understand the main determinants of the degree of countercyclicality of fiscal policy, we carry out the estimation of Eq. (10), where the coefficients of countercyclicality are estimated according to (1). In terms of estimation methodology, the regression follows Furceri and Jalles (2018) using an unbalanced sample of countries that have at least 20 years of consecutive observations via a weighted least-squares estimator.

Results suggest that coefficients associated with the various determinants are economically significant and typically exhibit the expected signs (Table 4). The levels of financial and economic development, government size and institutional quality all matter for determining the degree of countercyclicality of fiscal policy. For example, a one percentage point increase in the ratio of credit to GDP is associated with an increase in the fiscal countercyclicality coefficient ranging between 0.14 and 0.24 points (i.e., by about 1/4 standard deviation). Increasing real GDP per capita by one percentage point leads to an improvement of the fiscal countercyclicality coefficient that ranges between 0.09 and 0.16 points. Footnote 30 Government size proxied by total government expenditure ratio to GDP is statistically insignificant in the global sample. Higher debt levels are associated with an increase in the size of the fiscal countercyclicality coefficients. The fiscal countercyclicality coefficient increase by 0.02 and 0.05, respectively, for additional one percentage point increase in the gross debt ratio. With regard to institutional quality, increasing the margin of majority index by 1 point is associated with 0.06–0.1 percentage point increase in the fiscal countercyclicality coefficient. Similarly, this coefficient increases by 0.06–0.1 for each 1-point reduction in the government fractionalization. Both these variables point to political cohesion as a key factor for enhanced countercyclicality in line with the evidence provided in Fatas and Mihov (2013) and Lane (2003). These authors found that more constraints on the executive branch of the government tend to reduce government spending volatility and positively influence overall fiscal countercyclicality. In contrast, other political variables including measures of informality, corruption and governance, are not statistically significant. Finally, banking crises are positively related to fiscal countercyclicality.

Table 4 Key determinants of the countercyclicality of fiscal policy, 1990–2021The results are consistent with the relatively higher level of countercyclicality coefficients for AEs. This country group has higher levels of financial and economic development, larger government sizes and better institutional quality. At the same time, some of the set of covariates included in Eq. (10) tend to have different effects across country groups (Tables 5 and 6). For example, while trade and capital account openness are negatively correlated with fiscal countercyclicality in AEs (as found in Aghion and Marinescu 2008 and Furceri and Jalles 2018), they are positively associated with fiscal countercyclicality in emerging markets and low-income countries. Similarly, government size tends to have a larger effect in AEs than in developing economies, while the opposite is true for the level of economic and financial development.

Table 5 Determinants of fiscal countercyclicality for advanced economies, 1990–2021Table 6 Determinants of fiscal countercyclicality for emerging markets and developing economies, 1990–2021

The analysis can be further refined by investigating the specific determinants of automatic stabilizers (Table 7). For this purpose, we use (3) to decompose the coefficient \(^>>\) associated with automatic stabilizer component estimated in (2). Results show that the impact of financial and economic development on automatic stabilizers is relatively less pronounced than for the overall coefficient. Notable exceptions compared with results in Table 4 are the government size and the gross debt ratio, whose impact of automatic stabilization is more pronounced.

Table 7 Determinants of automatic stabilizers, 1990–2021Finally, as a robustness check, we apply alternative indicators and re-estimate the full specification in Table 4 by excluding country and/or time fixed effects (Table 8) and by splitting the country sample into high-debt versus low-debt countries (Table 9). Results are largely consistent with those in the baseline specification in Table 4 in terms of the statistical significance of the macroeconomic variables.

Table 8 Determinants of countercyclicality of fiscal policy, robustness check with alternative specifications

Table 9 A summary on the determinants of countercyclicality of fiscal policy: distinguishing between high- and low-debt countries

This paper revisited the notion of fiscal countercyclicality in light of recent business cycles and severe downturns. The main contribution of the paper is to provide a novel dataset of time-varying measures of fiscal countercyclicality for a large and unbalanced panel of advanced and emerging market and developing economies between 1980 and 2021. The paper investigated the scope, time trend and cross-country variation of the countercyclicality of fiscal policies, distinguishing the role between discretionary fiscal policy and automatic stabilizers, as well as the effects of different budget components. It also presents the main macroeconomic and structural determinants of fiscal countercyclicality. The use of time-varying measures of fiscal stabilization overcomes the major limitations of previous studies when assessing its determinants that rely on cross-country regressions without accounting for country-specific as well as global factors, such as the potential different effects during severe crises.

Our results show that: (i) the countercyclicality of fiscal policies has increased over time for many economies over the last two decades, particularly for emerging market economies; (ii) the countercyclicality tends to be much stronger during severe downturns and statistically different from typical recessions, especially for advanced economies; (iii) previously estimated coefficients on countercyclicality are likely to be lower bounds; (iv) the discretionary and automatic components of the budget balance display countercyclical effects for advanced economies, but cannot be pinpointed in a statistically significant way for emerging market economies and low-income countries; (v) the countercyclicality of fiscal policies operates primarily though the expenditure side of the budget, with social benefits being the most countercyclical component; and (vi) financial development, government size and institutional quality matter for the degree of countercyclicality.

These findings support the view that fiscal responses have been stronger during severe economic downturns, such as the COVID-19 pandemic and during the global financial crisis. Our results also confirm the importance of automatic stabilizers as part of the fiscal toolkits in responding to adverse shocks. From a policy perspective, the results suggest that better-developed financial systems and stronger institutional quality can promote stronger over fiscal countercyclicality. In particular, financial development and openness, government size and effectiveness, and social protection can strengthen automatic stabilizers. One limitation of our work is that it does not provide a benchmark for the optimal degree of fiscal countercyclicality.

In other words, by lessening the effects of the liquidity constraints faced by households and alleviating the impact of exogenous shocks to aggregate income on aggregate current consumption and output, fiscal stabilizers reduce output fluctuations because some components of fiscal accounts react automatically to the cycle, increasing public deficits in recessions and decreasing them in expansions.

This approach has been widely used by the OECD, the European Commission and the IMF country teams.This approach defines automatic stabilizers to be the cyclical component of the budget balance or its elements that is the automatic/cyclical change in the fiscal position (relative to GDP) resulting from a one percentage point change in the output gap. Semi-elasticities can also be estimated using a regression-based approach, in which case changes in components of the budget balance are regressed on changes in the output gap. While this approach allows for controlling for other factors, it can suffer from the endogeneity of the output gap.

The microeconomic approach, however, has limitations because it only accounts for the direct stabilizing role of the tax and benefit system and does not consider indirect stabilizing effects related to general equilibrium and behavioral responses.

A wide range of shocks have been considered in macro-simulation models: shocks to consumption, income, investment and productivity. Consumption and income shocks are found to have the largest stabilizing effects given their direct association with tax revenue (e. g.; Brunila et al. 2003; Tödter and Scharnagl 2004; European Commission, 2017b). Also, estimates of automatic stabilizers are typically larger for microeconomic stimulations than for reduced-form macroeconomic models. This difference in the strength of automatic stabilizers is primary explained by the fact that the macro approach accounts for general equilibrium effects arising from behavioral responses of firms, workers and consumers and feedback effect arising from a monetary policy response (Mohl et al. 2019).

For a recent contribution on the issue of public sector efficiency, see Afonso et al. (2022).When examining the cyclical properties of the budget balance, it is common to separate into the cyclical balance and the cyclically adjusted balance (Gali and Perotti 2003). Changes in the cyclical balance give an estimate of the budgetary impact of aggregate fluctuations through the induced changes in tax bases and certain mandatory outlays (that is, automatic stabilizers). Subtracting the cyclical balance from the overall budget balance would be the cyclically-adjusted balance.

For surveys on potential output estimation methods, see, for example, Ladiray et al. (2003); Horn et al. (2007); Bassanetti et al. (2010); Anderton et al. (2014); Alichi et al. (2017).

Table 10 in the appendix summarizes the variables definition.For instance, Fatás and Mihov (2012) found that the response of fiscal policy to cyclical fluctuations was relatively stronger in the post-1990 period when inflation was low and stable in most countries.

Financial development is proxied by the credit-to-GDP ratio in the regressions. Trade openness is proxied by the ratio of total exports and imports to GDP in the regressions. The regressions use the Chinn–Ito index of capital account openness (Chinn and Ito 2006).Government size can alternatively be measured by the size of the social expenditures in percent of GDP. Social spending is a key component of public spending and is also critical component of automatic stabilization, particularly in OECD countries (Darby and Melitz 2008).

Data on financial crises are based on the dataset in Leaven and Valencia (2018).For instance, Ma et al. (2020) study six modern health crises and find that countries that respond to pandemic shocks with higher government expenditures, especially on health care, tend to experience relatively stronger economic recovery. A dummy variable is included.

Those economies are particularly prone to tax evasion non-compliance and limited execution of expenditure comments.

The informality data are taken from Elgin et al (2021).Kose et al. (2020) provide a cross-country Database of Fiscal Space, which covers 202 countries over the 1990–2020 period and contains a variety of proxies for fiscal space. Two alternative proxies, namely general government gross debt and fiscal balance, both as ratios to average tax revenues, are used for robustness check.

The operation of escape clauses, by adding more flexibility, is likely to further improve countercyclicality.

We include a dummy indicating the existence of fiscal rules as an additional regressor. The sign of the coefficient on this dummy variable is unknown a priori, which depends on the existence of escape clauses allowing for more expansionary measures during severe downturns.

The Database of Political Institutions is used to get the dates for presidential and legislative elections. The World Bank’s Governance Indicators are used (note that in this case the data only begins in 1996), namely the Government Effectiveness and Regulatory Quality.

The margin of majority is the fraction of seats held by the government, relative to total seats (government plus opposition plus nonaligned). Parliamentary regimes and proportional representations are dummy variables indicating, respectively, if the political regime is parliamentary and if candidates are elected based on the percent of votes received by their party. The margin of majority is included in the baseline specification, whereas the dummy variables for parliamentary regimes and proportional representations are included in robustness checks.

The Corruption Perception Index from Transparency International was used to proxy for corruption. The CPI ranks 180 countries and territories around the world by their perceived levels of public sector corruption, scoring on a scale of 0 (highly corrupt) to 100 (very clean).

Using the primary fiscal balance instead of the overall fiscal balance leaves our main results unchanged.

We also use an alternative external instrument, namely the change in the export price index (Ilzetzki and Vegh 2008). The results are similar to those obtained from (i) and (ii).

The overall procyclically for LICs that emerges from Fig. 2 contrasts from the countercyclicality shown in Table 1. This apparently contrasting conclusion is due to a different samples the two exercises.

The first 10 years of the sample (1980–89) were therefore discarded. The resulting time-varying estimates are similar and comparable to those in Furceri and Jalles (2018) who used the varying-coefficient model proposed by Schlicht (2003). This model, as referred by its author, is a generalization of the standard linear model where the independent variables can (slowly) change over time (as opposed to remaining constant, as assumed in the linear model). As put by Jalles (2021), Schlicht’s method involves as estimation by a method of moments estimator that converges asymptotically with the maximum-likelihood estimator.

Estimating an error correction model (ECM) would be useful for differentiating between the short- and long-run elasticities of budget components. But results from unit-root tests suggest that most variables are stationary, and therefore, that estimating an ECM is not warranted in this setting.

However, it is worth noting that coefficient on GDP per capita turn negative and significant at the 10 percent level when inflation is introduced as an additional regressor (specification 7). This unexpected result is partly owing to a sharp drop in the sample size, from 3,224 in the baseline specification (specification 1) to 774 (specification 7).

Open access funding provided by FCT|FCCN (b-on). The funding was provided by Fundação para a Ciência e a Tecnologia